Sri Lanka’s economy seen as a ‘ticking time bomb’

Sri Lanka’s COVID-stricken economy is being likened to a ticking time bomb that could go off at any moment as foreign reserves plummet, the cost of living rises and the central bank carries on printing money.

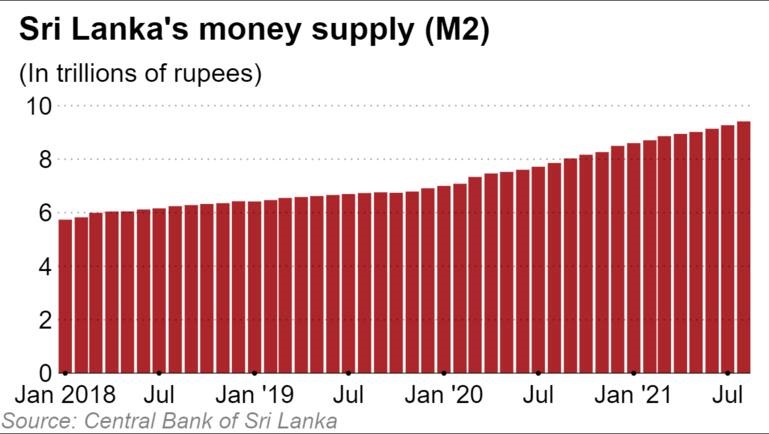

The Central Bank of Sri Lanka printed over 130 billion rupees ($640 million) in October alone, but that is just the iceberg’s tip. From December 2019 to August 2021, Sri Lanka’s money supply increased by 2.8 trillion rupees — a massive 42%.

Much of the money went to pay the salaries of 1.2 million state sector employees, and to cover pensions that each year cost the government a thumping one trillion rupees. Unlike the private sector, which suffered salary cuts during the COVID-19 pandemic, state employees carried on at full pay despite the empty public coffers. Money was also printed with a view to keeping interest rates low.

Though it has generally been characterized as printing money, most of the increase in the overall money stock — or “broad money” as it is termed — since the end of 2019 is made up of government borrowings from the central bank and commercial banks.

Addressing a press conference earlier this month, Central Bank Governor Ajith Nivard Cabraal defended the decision to print money on the grounds that it was needed to maintain stability.

“If you read the monetary law, one of the responsibilities of the central bank is price stability as well as financial system stability,” he said. “Sometimes, in the interest of financial system stability — as well as economic and price stability — there can be instances where additional treasury bills could be issued to the government.”

Cabraal said similar money supply increases have been seen in about 120 countries “as a result of the pandemic.”

This view is not acceptable to W. A. Wijewardena, a former central bank deputy governor. He has warned that the 42% increase will pump severe inflation, possibly to over 40% in the next few years.

“Normally a central bank can allow this money stock to increase without causing inflation if the increase is equivalent to the real growth of the economy,” Wijewardena told Nikkei Asia. Since growth in 2020 was -3.6% and is expected to be around 4.5% in 2021, real net growth for the two years will be “about 1%,” he said.

It was Wijewardena who used the economic time bomb analogy: “It is now ticking and can go off at any time,” he told Nikkei.

Sirimal Abeyratne, an economics professor at the University of Colombo, is more supportive of the current monetary policy because of the fiscal damage the pandemic has caused. The extra money has helped fund government spending and kept interest rates down for private credit.

But he thinks the approach should be “only temporary,” and notes that the central bank actually tightened monetary policy in September when inflationary signals were detected. He told Nikkei that a price has also been paid “in terms of exchange rate pressure.”

Sergi Lanau, deputy chief economist at the Washington-based Institute of International Finance, has taken a similar view. Sri Lanka’s central bank was compelled to finance the government’s significant expenditure during the pandemic, “which was not unusual.” The central banks of the Philippines and of Indonesia did much the same. But he cautioned that “if money printing continues, we can expect pressure on inflation and on the exchange rate, which does not help resolve the ongoing crisis.”

Cabraal told the press conference that higher inflation is a concern. “We are conscious of that and we will manage it,” he said. “We don’t want to see a situation where inflation could rise unduly.” He predicted “a slight dip” in December, and said the central bank intended to ensure price rises do not accelerate into double digits.

In mid-October, Colombo lifted price controls on essential food items, including household gas. That saw the the price of a 12.5 kilogram cylinder of cooking gas jump from 1,400 rupees to 2,675 rupees in the space of a week. A 400 gram pack of milk powder, a staple in almost every Sri Lankan home, increased to 480 rupees from 380 rupees, and wheat flour went up by 10 rupees a kilo causing a domino effect in bread and other flour-based products.

Last week, the Lanka Indian Oil Company, which competes with the state-run fuel distributor Ceylon Petroleum Corporation (CPC), announced a 5-rupee increase per liter of fuel with effect from Oct. 21. CPC has since been seeking approval to increase fuel prices after suffering a loss of 70 billion rupees this year up to August.

Sri Lanka’s inflation rate has increased this year from around 4% to about 7%, but fell back slightly in September. The September food index was meanwhile up 22% compared to two years earlier.

Abeyratne said the price increases were in large part due to ad hoc and piecemeal policy decisions.

In 2019, soon after President Gotabaya Rajapaksa was elected president, sweeping tax cuts were announced to make good on an election pledge. The bonanza included cutting value-added tax to 8% from 15%, and abolishing the 2% nation-building tax on domestic goods and services.

Whilst the government blames the pandemic for the economic reversal, Eran Wickramaratne, a former state minister of finance, considers the tax cuts to be one of the main causes.

“The financial crisis was brought on soon after President Rajapaksa did away with taxes, and following their removal government revenue fell by nearly 30% in 2020,” he told Nikkei. “The government created the financial crisis itself, but certainly the pandemic made it more complicated, resulting in total mismanagement of the economy.”

In 2020, government revenue in Sri Lanka amounted to approximately 9.6% of the nation’s gross domestic product, down from 12.6% in 2019 ahead of the tax cuts.

Both local and international economic experts, including Lanau and Wijewardena, insist that the only way out now is for Sri Lanka to turn to the International Monetary Fund.

Wijewardena said that an IMF special drawing rights loan facility of about SDR 2 billion ($2.8 billion) at a rate of 3.55% repayable over 4.5 to 10 years would help Sri Lanka recover foreign investor confidence and buttress foreign exchange flows. That would provide a breathing space to introduce necessary long-term economic reforms to return the country to growth.

“The financial crisis was brought on soon after President Rajapaksa did away with taxes, and following their removal government revenue fell by nearly 30% in 2020,” he told Nikkei. “The government created the financial crisis itself, but certainly the pandemic made it more complicated, resulting in total mismanagement of the economy.”

In 2020, government revenue in Sri Lanka amounted to approximately 9.6% of the nation’s gross domestic product, down from 12.6% in 2019 ahead of the tax cuts.

Both local and international economic experts, including Lanau and Wijewardena, insist that the only way out now is for Sri Lanka to turn to the International Monetary Fund.

Wijewardena said that an IMF special drawing rights loan facility of about SDR 2 billion ($2.8 billion) at a rate of 3.55% repayable over 4.5 to 10 years would help Sri Lanka recover foreign investor confidence and buttress foreign exchange flows. That would provide a breathing space to introduce necessary long-term economic reforms to return the country to growth.

– Nikkei Asia